Kind of, but not exactly. Let me try and see if I can simplify it a bit:

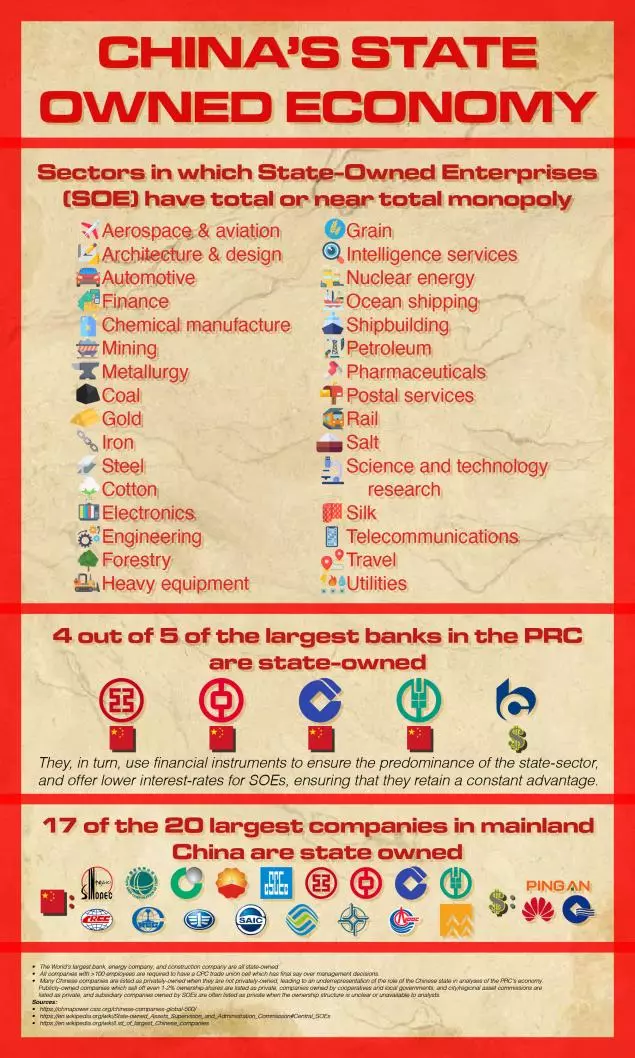

China already has the world’s largest industrial capacity (31% of the world’s manufacturing capacity, compared to 18% in the US, and 5% for the EU and Japan each). There is no need for China to accumulate US dollars in order to finance its own development. That also means, there is no need for China to suppress its wages to make exports competitive (for the record, the average working class purchasing power in China is half that of the average working class in South Korea).

From an MMT perspective, the People’s Bank of China can simply create the currency needed to develop all these amazing cities, technologies, infrastructure like high speed rails etc.

However, the Chinese economic model (very neoliberal brained) is still stuck to very much to the model IMF has been recommended to developing countries - balance your budget (keep budget deficit within 3%), don’t spend more than what you can earn. This means that in order to finance internal development, you have to either earn foreign reserves (export goods to Western countries), or borrow from financial institutions (banks).

For the former, a Chinese exporter sells goods to the US importer, earning US dollars in its US bank account. The Chinese exporter can now do three things:

- Use the dollar it earned to import goods/services sold in US dollar (trade for real goods/services)

- Use the dollar it earned to buy US securities (to earn interests)

- Convert the earnings to yuan and use the money to pay its workers, invest in its business locally etc.

For the third option, the exporter sells the US dollars (in its US bank accounts) to the PBoC, who in turns uses the dollar to buy US treasuries or other dollar-denominated securities. This becomes the foreign reserves of the PBoC. Note that all of the dollar transactions involved never leaves US shores and always takes place within the US banking system.

In turn, the PBoC creates an equivalent amount of yuan (backed by the dollar it just purchased from the exporter) in the Chinese bank account of the Chinese exporter, who can now in turn use the yuan to pay its workers and invest etc.

The other way is to borrow from financial institutions, either foreign or local. But note that the loans that are created also have matching liabilities + interests. If you borrow 100k yuan, you have to pay back 100k to the lender + interest payment. No new net financial asset is created in this process. (Note that this is the primary mode of investment in China today that weighs just as much as the central bank creating new money from export earnings, and it is becoming a big issue for the solvency of many local banks and local/municipal governments)

So, the more goods you export to the US, the more foreign currencies you accumulate, the more you can convert them into local currencies to spend locally. This is why developing countries run trade surplus, such that they can accumulate foreign currencies (the US simply prints its dollars out of thin air, without having to contribute anything tangible to the global) and finance their own development. This allows them to stay within the 3% budget deficit as imposed by the IMF, and using the trade surplus earnings to cover for their expenditures. And so, to keep their exports competitive, you as a developing country will always have to make sure your currency exchange rate is lower, suppress labor wages etc. to maintain that competitive advantage. This is also the so-called “middle income trap” - developing countries cannot make the leap into high income countries because they have been told to keep earning export revenues to finance their own domestic development.

MMT says this is nonsense. MMT says that a government with monetary sovereignty (that creates its own currency, is not running a fixed exchange rate where its currency is pegged to a metal or another currency) can always finance its own development so long as it is backed by the availability of labor, resources, and technology.

That means if you’re a poor developing country that has to import food and energy, usually kept impoverished by global imperialist institutions like the IMF and World Bank, you simply cannot create the money as you wish. But for China, it’s a different story - there may be food and raw resources that China has to import - but it still has the world’s largest industrial capacity and is technologically self-sufficient to not have to rely on advanced machineries from wealthy Western imperialist countries to keep their lights on.

However, because the Chinese economists are all Western educated, neoliberal brained, they continue to stick to this model, orientating their economy to one that is heavily reliant on export-led growth. In other words, using Chinese labor and resources to send cheap goods to Western countries and get a bigger number in their bank statement in return.

This was all going well in the 2000s as China became the world’s factory and enjoyed double digit growth. Then, the 2009 GFC happened, and starting from the US consumers, but soon spread across the world, the slump in consumption would hit the Chinese export-oriented economy hard.

To mitigate the crisis, the Chinese central government prioritized infrastructure building domestically, to absorb the loss in export revenues. This culminated in the infamous 4 trillion yuan stimulus, most of which financed by bond issuance. And it did work - not only did China not experience global recession, due to the timely reallocation of economic activity into construction, but even saved the surrounding economies from complete disaster. For example, Australia was saved by China’s infrastructure building phase due to increasing demand of imported raw materials.

Now, before we move on, I need to introduce the unique style of Chinese governance. As opposed to the stereotype that present day China is run by dictators with a centralized bureaucracy, the matter of fact is that Chinese economy is highly decentralized. Local governments contribute nearly half of the national tax revenues, and 70-85% of the budget expenditures. The central government in Beijing, in turn, controls the local governments through its authority to promote local officials. So Beijing sets a goal for promotion, the local officials work to meet that goal in order to get promoted. One of the main performance indicator is GDP growth, and this will become very important later on.

The decentralization of authority was one of the most significant changes under Deng’s reform, but the key event that would precipitate in the property market bubble today was the 1994 Tax-Sharing Reform, that conferred local governments with the authority of land financing.

So, back to 2009, with export revenues falling, the local governments began to find themselves under financial strain. Their inability to pay back outstanding debt also denied them from obtaining fresh credits from the financial institutions. Furthermore, the cut in GDP growth numbers almost certainly meant that they’re going to miss the score needed for promotion.

The 4 trillion yuan stimulus aimed at infrastructure building came at just the right time, for local governments with the power of land financing. The keep the GDP growth numbers up, local governments bet on leasing/selling land initially owned by the state to drive up revenue.

The schemes are extremely varied, “innovative” and complex to skirt various laws and legal enforcements, but it follows the general pattern: local governments would use its state authority to pressure financial institutions (local banks) to release loans to property developers, who would use the loans to finance building new cities, housing, infrastructures, high speed rail, you name it. The local governments would then bet on the land value to rise with development, and the revenues earned from selling/leasing the land at high price would pay off the debt they have borrowed to finance public utilities/domestic development.

The reason we know all this in explicit detail, ironically, is because of the Evergrande’s court case. But the investment in infrastructure building under the relationship formed under trifecta of local governments-financial institutions-property developers would become a primary mode of sustaining GDP growth in the face of falling export revenues. Many local officials made the career promotions of their lifetime during this period.

Because local governments were not allowed to issue debt, from 2009-2015, the borrowing was initially performed by the local governments setting up the Local Government Financing Vehicles (LGFV, effectively shadow banks). The borrowing that took place under this period would build up the so-called “hidden debt”, because they are not included in official accountings.

By the mid-2010s, it became apparent that the hidden debt problem is running out of control. We still don’t know the exact amount of cumulative hidden debt to this day, either because the government is worried about a market panic should the true number be revealed, or because even the central government has lost tracked of them. In either case, the amount has to be huge.

And so by 2015, the central government became fed up with the local government’s reckless hidden debt problem, and directly conferred the local governments with the authority to issue bonds/debt themselves. In other words, the central government no longer want to keep “bailing out” the excessive debt taken out by the local governments. You want to borrow, you shall be responsible for paying them yourselves.

(continued in the next comment)

{kind=link}